Reducing E&O Risk in Commercial Submissions: One Input, Zero Transcription Errors

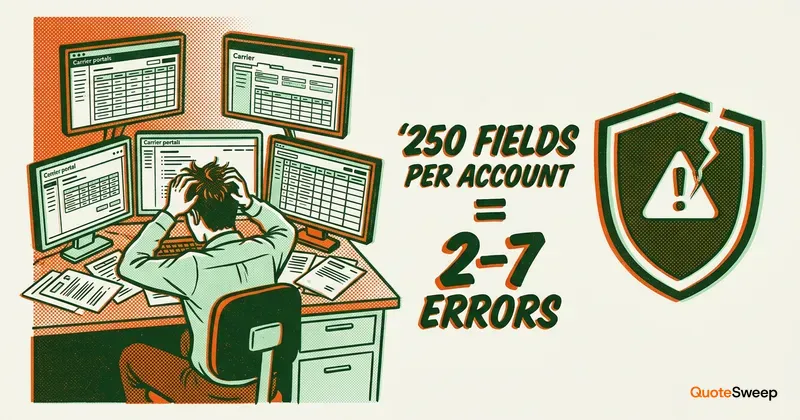

A commercial insurance submission to five carriers requires entering approximately 50 data fields per carrier portal – entity name, FEIN, business description, revenue, employee count, class codes, property values, prior insurance, claims history, coverage limits, deductibles, and dozens of supporting details. Five carriers times 50 fields equals 250 manual data entries for a single account. Ten carriers equals 500.

The widely studied human error rate for manual data entry is 1% to 3% under normal working conditions. At 250 entries per account, that translates to 2 to 7 errors per submission cycle. Most of those errors are harmless – a transposed phone digit, a slightly off address. But some of them aren't. A wrong class code changes the premium and the coverage scope. A wrong revenue figure produces a quote that won't survive an audit. A wrong entity type means the Named Insured is wrong on the policy.

Each of those errors is a potential errors and omissions claim waiting to happen.

TLDR: Manual re-entry of client data across carrier portals is the largest single source of preventable E&O exposure in commercial insurance submissions. At 50 fields per carrier and a 1-3% human error rate, submitting to 5 carriers produces 2-7 transcription errors per account. The errors that matter – wrong class codes, wrong revenue, wrong entity types – produce incorrect quotes that lead to audit surprises, coverage gaps, and E&O claims. Prevention requires reducing the number of times data is manually entered: ACORD form pre-fill, submission checklists, and single-input multi-carrier quoting tools that eliminate re-entry entirely.

How Transcription Errors Become E&O Claims

Our comprehensive guide to E&O risk reduction covers the full landscape of E&O exposure for insurance agents – failure to procure, inadequate coverage recommendations, failure to advise of policy changes. This article goes deeper on one specific category: errors that originate in the submission process itself. These errors are particularly insidious because they happen silently. The CSR doesn't realize the mistake. The carrier doesn't catch it (they assume the data the agent provided is accurate). The client doesn't know their policy was written with wrong information. Everyone discovers the error at the worst possible moment – when there's a claim.

The Chain of Consequences

Here's how a transcription error becomes an E&O claim, step by step:

1. Data entry error occurs. The CSR enters $1.2 million in revenue on one carrier portal but types $1.2 thousand – $1,200 – on another. Or they select class code 41677 (computer consulting) instead of 41675 (IT network installation) – similar numbers, very different risks.

2. The carrier quotes based on wrong data. The quote comes back at a premium that reflects the incorrect information. If revenue was understated, the premium is artificially low. If the class code is wrong, the premium reflects a different risk profile.

3. The policy is bound on incorrect information. The client accepts the quote, the agency binds the policy, and coverage incepts. Everyone is happy – the premium looks good.

4. An audit or claim reveals the error. For workers comp and general liability policies, the carrier conducts an annual premium audit. When the audit reveals that actual revenue is $1.2 million (not $1,200), or that the operations are IT network installation (not computer consulting), the carrier issues an additional premium bill. For significant discrepancies, the carrier may also question whether the policy was obtained through material misrepresentation.

5. The client is surprised and angry. The client receives a $15,000 additional premium bill they didn't expect. They call the agent. The agent reviews the file and discovers the transcription error.

6. The E&O claim follows. The client alleges the agent misquoted the policy, causing them to bind coverage based on incorrect pricing and potentially incorrect coverage terms. The agency's E&O carrier opens a claim.

This chain plays out across agencies every year. The specific errors vary, but the pattern is consistent: manual data entry creates the error, nobody catches it during the quoting process, and the consequences surface months later.

The Most Dangerous Transcription Errors

Not all errors carry equal E&O risk. These are the transcription errors most likely to result in claims, audits, or coverage disputes.

Wrong Class Code

Class codes drive everything in commercial insurance: premium calculation, coverage scope, carrier eligibility, and audit exposure. A wrong class code on a general liability or workers compensation policy doesn't just change the price – it changes what the carrier thinks they're insuring.

Example: A general contractor (ISO CGL class code 91580) is entered as a handyman (class code 91340). The GL premium for a general contractor with $2 million in revenue might be $8,000 to $12,000. For a handyman, it might be $2,500 to $4,000. The quote comes back at $3,200. The client is thrilled. At audit, the carrier reclassifies to general contractor and bills an additional $6,000 to $8,000. If the client had a claim during the policy period, the carrier may also dispute coverage because the risk was misrepresented on the application.

Why this happens in re-entry: Class code fields are numeric. Transposing two digits, selecting the wrong entry from a dropdown, or misremembering a code from one portal to the next is easy. When you're entering the same account into five portals in succession, the class code field is just one of 50 fields, and fatigue increases error rates on repetitive tasks.

Wrong Revenue or Payroll

Revenue and payroll are the primary rating bases for general liability and workers compensation, respectively. Getting them wrong produces quotes that are mathematically incorrect.

Example: A restaurant reports $800,000 in annual revenue. The CSR enters $800,000 in the first carrier portal. In the second portal, fatigue or distraction leads to $80,000. The second carrier's quote comes back significantly lower. If that carrier is selected and the policy is bound, the audit will reveal an 10x discrepancy in reported revenue, triggering a massive additional premium.

The audit math: Workers comp and GL policies are auditable. The carrier will compare reported payroll and revenue against actual figures. Underreporting by any significant percentage triggers an additional premium bill. If the underreporting was due to agent error rather than client fraud, the E&O exposure falls on the agency.

Wrong Entity Type

Entering "Sole Proprietorship" when the client is an LLC – or "Corporation" when they're a Partnership – affects who is insured under the policy. The Named Insured definition varies by entity type, and a policy issued to the wrong entity type may not provide coverage to the right people or may provide coverage to people who shouldn't be included.

Example: A two-person partnership is entered as a corporation. The policy is issued with a corporate Named Insured. When one of the partners is personally sued for a negligent act during business operations, the policy may not respond because the individual partner isn't an insured under a corporate entity policy – the corporation is.

Missing or Wrong Prior Insurance

Carriers use prior insurance as an underwriting factor. A client with continuous coverage is a different risk profile than a client with a gap in coverage. Incorrectly reporting prior insurance – or failing to report it – can result in policy rescission if the carrier discovers the misrepresentation.

Example: The client had prior coverage with Carrier A, which the CSR correctly enters in Portal 1. In Portal 3, the CSR accidentally selects "No Prior Insurance" from a dropdown. The carrier issues a quote and binds the policy. When a claim occurs, the carrier investigates and discovers the misrepresentation. Depending on the jurisdiction and the materiality of the misrepresentation, the carrier may void the policy – leaving the client uninsured for the claim and the agency exposed to an E&O action.

Wrong Prior Claims History

Understating or omitting prior claims has similar consequences to wrong prior insurance information. Carriers rate partially based on claims history. A clean claims history produces a lower premium. If a claim surfaces that wasn't reported on the application, the carrier may rescind or impose a retroactive surcharge.

The problem with manual re-entry: When entering claims history into five different portals, each with its own format for reporting claims (some ask for date/type/amount, some ask for paid/reserved/status, some use dropdowns and some use free text), the opportunities for inconsistency multiply. Claim A gets reported in Portals 1 through 3 but is accidentally omitted from Portals 4 and 5.

Quantifying the Risk

Let's put real numbers on the E&O exposure created by manual submission workflows.

The Error Probability Math

| Carriers Submitted To | Fields Per Carrier | Total Manual Entries | Expected Errors (1% rate) | Expected Errors (3% rate) |

|---|---|---|---|---|

| 3 | 50 | 150 | 1.5 | 4.5 |

| 5 | 50 | 250 | 2.5 | 7.5 |

| 8 | 50 | 400 | 4.0 | 12.0 |

| 10 | 50 | 500 | 5.0 | 15.0 |

Most of these errors won't trigger claims. A wrong phone number doesn't create E&O exposure. But when you're making 250 to 500 manual entries per account and 5 to 15 of them are wrong, the probability that one of those errors hits a consequential field – class code, revenue, entity type, claims history – is not negligible. Across a year of commercial submissions, the cumulative exposure adds up.

What E&O Claims Actually Cost

According to industry data, the average E&O claim costs over $50,000 in combined defense costs and settlement. Complex claims – particularly those involving coverage rescission or significant audit adjustments – can exceed $200,000. These figures include:

- Defense costs: $15,000 to $50,000+ in legal fees, even if the claim is ultimately dismissed

- Settlement or judgment: Variable, but often $20,000 to $150,000+ for claims involving material misrepresentation

- Indirect costs: Time spent responding to the claim, damage to client relationships, potential impact on the agency's own E&O renewal premium

And the trend is not favorable. Professional liability claims have increased 57% over the past decade, with both frequency and severity rising. Clients are more likely to pursue claims, and attorneys are more aware of the recoveries available from agency E&O policies.

Your E&O Premium Is a Tax on Manual Processes

Here's the contrarian take that most agency owners haven't considered: your E&O premium is, in significant part, a tax on the manual processes your agency uses for commercial submissions.

E&O underwriters price agency E&O coverage based on the agency's risk profile – claims history, revenue, lines written, procedures, and controls. An agency that manually re-enters data into 10 carrier portals for every commercial submission has a structurally higher error rate than an agency that enters data once and auto-fills across carriers. The first agency is statistically more likely to produce the kinds of transcription errors that become E&O claims. Over time, that higher claims frequency shows up in the E&O premium.

Investing in tools that eliminate manual re-entry doesn't just save CSR time – it reduces the error rate that drives E&O claims, which can reduce the E&O premium that the agency pays. Some agency E&O carriers explicitly ask about submission procedures and technology during the underwriting process. An agency that can demonstrate a single-input workflow, automated data validation, and systematic submission tracking is a better risk than one that relies on CSRs manually typing the same data into portal after portal.

The irony: agencies often view E&O premiums as a fixed cost of doing business while simultaneously refusing to invest in the tools that would reduce the risk those premiums cover. The premium isn't fixed – it's a function of the agency's error exposure, and the error exposure is a function of how many times human hands touch the same data.

Prevention Strategies

Reducing transcription-related E&O risk requires reducing the number of times data is manually entered. Here are the strategies, ordered from least to most effective.

Strategy 1: Submission Checklists (Moderate Impact)

A pre-submission checklist ensures that key data points are verified before any carrier portal entry begins. The checklist doesn't prevent transcription errors during entry, but it catches errors in the source data.

Commercial Submission Pre-Flight Checklist:

- Entity name verified against formation documents (not just the client's verbal description)

- FEIN confirmed (not estimated or recalled from memory)

- Class code verified against actual operations (not just the client's self-description)

- Revenue confirmed against financial statements or tax returns

- Payroll confirmed and allocated by class code

- Prior insurance verified via loss runs (not client self-report)

- Claims history complete and accurate (dates, types, amounts, status)

- Property values validated with replacement cost estimator

- All ACORD forms complete with no blank fields

- Effective date confirmed with client

This checklist catches errors in the input data. It doesn't prevent the CSR from mistyping that data into a carrier portal, but it ensures the starting point is accurate.

Strategy 2: ACORD Form Pre-Fill (High Impact)

Using a completed ACORD 125 as the single source document for all carrier submissions creates one verified data set that the CSR references for every portal entry. This is better than entering data from memory or from scattered notes, but it still requires the CSR to manually transfer data from the ACORD form into each portal.

How to implement:

- Complete the ACORD 125 (and line-specific supplementals) first, before touching any carrier portal

- Have a second person verify the completed ACORD against the client's source documents

- Use the verified ACORD as the only reference for carrier portal entries – never enter data from memory or from raw client documents

The improvement: instead of 250 manual entries from scratch, the CSR makes 250 manual entries from a verified reference document. Error rate drops from 1-3% (entering from memory) to a lower rate (copying from a reference), but errors still occur – particularly transposition errors, dropdown selection errors, and fatigue-related mistakes on repetitive fields.

Strategy 3: Copy-Paste Standardization (Moderate-High Impact)

For fields that accept free text – operations descriptions, loss narratives, address information – standardize the practice of copying and pasting from the ACORD form or AMS rather than retyping. This eliminates transposition errors on text fields.

Limitations: Many carrier portal fields are dropdowns, radio buttons, or formatted inputs that don't accept paste. Class codes, entity types, state selections, and yes/no fields must be manually selected in each portal. These are precisely the fields where transcription errors are most consequential.

Strategy 4: Single-Input Multi-Carrier Quoting (Highest Impact)

A multi-carrier quoting tool fundamentally changes the error equation. Instead of entering data into each carrier portal manually, the CSR enters data once. The tool maps that single data entry to each carrier's required format and submits through parallel quoting to all selected carriers simultaneously.

The math changes:

| Approach | Data Entries | Error Opportunities | Consequential Error Risk |

|---|---|---|---|

| Manual, 5 carriers | 250 | 2-7 errors | Moderate-High |

| ACORD pre-fill, 5 carriers | 250 (from reference) | 1-4 errors | Moderate |

| Single-input tool, 5 carriers | 50 (one entry) | 0.5-1.5 errors | Low |

Single-input quoting reduces error opportunities by 80% compared to manual entry. The data is entered once, verified once, and transmitted consistently to every carrier. There's no opportunity for the class code to be right on Portal A and wrong on Portal B, because there's only one entry.

Additional E&O benefits of single-input tools:

- Automatic data validation. Many tools flag common errors – revenue that seems too low for the class, class codes that don't match the operations description, missing required fields – before submission. Manual portals accept whatever you type.

- Consistent submissions. Every carrier receives identical data. In an E&O investigation, consistent submissions across carriers demonstrate that the agent provided the same information everywhere – there's no discrepancy to explain.

- Audit trail. The tool logs what data was entered, when, by whom, and what was submitted to each carrier. This documentation is exactly what an E&O carrier wants to see during a claim investigation.

Documentation Requirements Your E&O Carrier Expects

Regardless of your submission technology, your E&O carrier expects certain documentation practices. Meeting these expectations demonstrates procedural discipline and can favorably influence your E&O renewal.

What to Keep in Every Submission File

- Completed ACORD forms – signed by the client, with no blank fields

- Source documents – loss runs, financial statements, or other documents used to verify client data

- Carrier submissions – copies of what was submitted to each carrier, or a log showing which carriers received submissions and when

- Quotes received – all carrier responses, including declines, with dates

- Comparison documentation – the analysis used to compare options and arrive at a recommendation

- Client communication – emails or documented calls presenting options and capturing the client's decision

- Binding confirmation – written confirmation from the carrier and written confirmation to the client

What to Document When Errors Are Discovered

If you discover a transcription error after submission or binding:

- Correct the error immediately with the carrier

- Document what the error was, when it was discovered, and how it was corrected

- Notify the client if the correction affects their premium, coverage, or policy terms

- Document the client notification and their acknowledgment

- Review the process to determine how the error occurred and what procedural change prevents recurrence

- Report to your E&O carrier if required by your policy terms (some E&O policies require notification of known errors even before a claim is made)

Proactive error correction – finding and fixing mistakes before they become claims – is strongly viewed as a positive by E&O underwriters. An agency that discovers and corrects errors demonstrates oversight. An agency that only discovers errors when a client files a claim demonstrates the opposite.

Building a Culture of Accuracy

Technology and checklists reduce errors, but culture determines whether those tools get used consistently.

Second-Set-of-Eyes Review

For high-value accounts or complex submissions, have a second CSR review the completed ACORD forms and carrier entries before submission. This is the same principle that aviation and medicine use – critical processes benefit from redundant checks. The time cost is 5 to 10 minutes per account. The E&O cost of a missed error is $50,000+.

Obviously, this isn't scalable for every small commercial submission. Reserve the second review for accounts above a premium threshold (say, $10,000) or in high-complexity classes. For more on how to structure CSR workflows and where automation can help with capacity, see our analysis on hiring a CSR vs. automating.

Error Tracking

Track transcription errors when they're discovered – whether you catch them before submission, the carrier catches them, or (worst case) they surface at audit or claim. Over time, this data reveals patterns: which fields are most error-prone, which CSRs may need additional training, and which carriers' portals are most confusing.

Most agencies don't track this because they don't discover the errors. That's precisely the problem. Implementing quality controls – random audits of submitted applications, comparison of ACORD forms against carrier portal entries, review of audit results for discrepancies – surfaces errors that would otherwise go undetected until they become claims.

Training on High-Risk Fields

Not all fields carry equal E&O weight. Focus training and quality controls on the fields where errors have the most severe consequences:

- Class codes – verify against actual operations every time

- Revenue and payroll – confirm against financial documents

- Entity type – verify against formation documents

- Prior insurance and claims – confirm with loss runs

- Property values – validate with replacement cost tools

- Named Insured – exact legal entity name, correctly spelled

These six categories represent perhaps 10% of the fields on a carrier application but account for a disproportionate share of E&O exposure. A CSR who gets these six right every time – even if they occasionally mistype a phone number or secondary contact name – has dramatically reduced the agency's transcription-related E&O risk.

The Agency KPIs That Track Submission Accuracy

If you're serious about reducing submission-related E&O risk, measure it. Our guide to insurance agency KPIs covers the full range of metrics agencies should track. For submission accuracy specifically, these metrics matter:

- Audit adjustment rate: What percentage of audited policies result in additional premium? A high rate may indicate systematic underreporting – often caused by transcription errors.

- Carrier information requests: How often do carriers request additional or corrected information after submission? Frequent requests suggest incomplete or inaccurate submissions.

- Quote-to-bind accuracy: How often does the bound premium match the quoted premium? Discrepancies often trace back to data that changed between quote and bind – sometimes because the original quote data was wrong.

- E&O claim frequency: Track claims over time. Any claim related to submission data should trigger a process review.

Frequently Asked Questions

What types of transcription errors are most likely to result in E&O claims?

The errors with the highest E&O risk are those that affect coverage scope or pricing: wrong class codes (which change what the carrier thinks they're insuring), wrong revenue or payroll figures (which produce incorrect premium at audit), wrong entity types (which affect who's insured under the policy), and omitted or incorrect claims history (which can trigger policy rescission for material misrepresentation). Errors on administrative fields – contact information, secondary addresses, phone numbers – rarely generate claims on their own, though they can complicate the claims process if the carrier can't reach the insured.

How many times does a CSR typically re-enter the same data during a commercial submission?

For a standard manual workflow, the same core data set is entered once per carrier portal. Submitting to 5 carriers means entering the client's information 5 separate times. Submitting to 8 carriers means 8 times. Each entry involves approximately 50 fields, so 5 carriers equals roughly 250 manual entries and 8 carriers equals roughly 400. A multi-carrier quoting tool reduces this to a single entry of approximately 50 fields, with the tool handling the mapping and submission to all carriers.

Can my agency's E&O premium be reduced by adopting better submission technology?

Yes, though the impact depends on your E&O carrier's underwriting approach. Many E&O carriers evaluate an agency's procedures and controls during the underwriting process. An agency that demonstrates single-input submission workflows, automated data validation, and documented quality controls presents a lower risk profile than one relying entirely on manual portal entry. Some carriers offer premium credits for formal risk management programs. Even without an explicit credit, a lower claims frequency over time will improve your loss ratio, which directly influences renewal pricing. The ROI calculation should include both the time savings from reduced manual entry and the potential E&O premium impact.

What should I do if I discover a transcription error after the policy has already been bound?

Contact the carrier immediately to correct the error. Most carriers will process a mid-term correction – especially if the agency identifies the error proactively rather than waiting for an audit or claim. Document the correction thoroughly: what the error was, when it was discovered, what the correct information is, and confirmation from the carrier that the policy has been updated. Notify the client if the correction affects their premium or coverage terms. File the documentation in the client record. If the error could have affected coverage during the period it was in force, consult with your E&O carrier about whether notification under your own E&O policy is required.

Is it realistic to eliminate all transcription errors in commercial submissions?

No. Zero errors is an aspiration, not a realistic target. Humans make mistakes, and even the best processes have failure modes. The goal is to reduce the frequency of consequential errors to the lowest achievable level and to have systems in place that catch errors before they become claims. Single-input quoting reduces error opportunities by approximately 80%. Submission checklists and second-set-of-eyes reviews catch many of the remaining errors. But some will slip through. The final line of defense is robust documentation – showing that the agency had procedures, followed them, and acted in good faith. That documentation doesn't prevent the error, but it dramatically improves the agency's position if the error leads to a dispute.