AI in the Insurance Agency: What Works

AI in insurance is real. But the gap between what AI vendors promise and what AI actually delivers inside an independent agency is wide enough to drive a truck through. Most agents have sat through webinars or conference presentations where someone demonstrated a futuristic vision of AI handling everything from quoting to claims. Then they go back to their office and spend the next hour manually entering the same client data into six different carrier portals.

This guide separates what AI genuinely does in independent insurance agencies today from what is still aspirational. No hype, no vendor talking points – just what works, what is getting close, and what agents should actually spend money on. For a focused look at AI in the quoting process specifically, see our AI insurance quoting reality check.

TLDR: AI in insurance agencies works well for document extraction, appetite matching, field mapping, and basic communication drafting. It does not generate quotes, replace underwriting judgment, or handle complex risk placement. The practical ROI comes from time savings on repetitive tasks – not from replacing agents. Focus your AI spending on tools that save your staff hours per day on data entry, not on tools that promise to transform your business model.

AI That Actually Works in Agencies Today

These are the AI applications that are shipping in production tools, being used daily by real agencies, and delivering measurable time savings. They are not theoretical or "coming soon" – they work now.

Document Extraction and OCR

AI-powered optical character recognition (OCR) and natural language processing (NLP) can read insurance documents – ACORD forms, loss runs, declarations pages, certificates of insurance, driver schedules – and extract structured data from them.

What it does: Instead of a CSR manually reading a 5-page loss run and typing claim dates, amounts, descriptions, and statuses into a spreadsheet or carrier portal, AI reads the document and populates the fields automatically. It handles ACORD 125s, 126s, 130s, and other standard forms. It reads dec pages from multiple carriers with different formats. It extracts loss history from carrier-specific loss run formats.

How well it works: For typed or digitally generated documents, extraction accuracy is consistently above 90% and improving. Handwritten entries, poor scan quality, and unusual document formats still cause errors. The practical approach is to use AI extraction as a first pass and have a human review the output – which is still dramatically faster than entering everything manually.

Where to find it: Most modern comparative raters and quoting tools include some form of document extraction. Standalone tools like Canopy Connect, Indio, and Fenris specialize in insurance data extraction. Some AMS platforms are adding extraction capabilities to their document management modules.

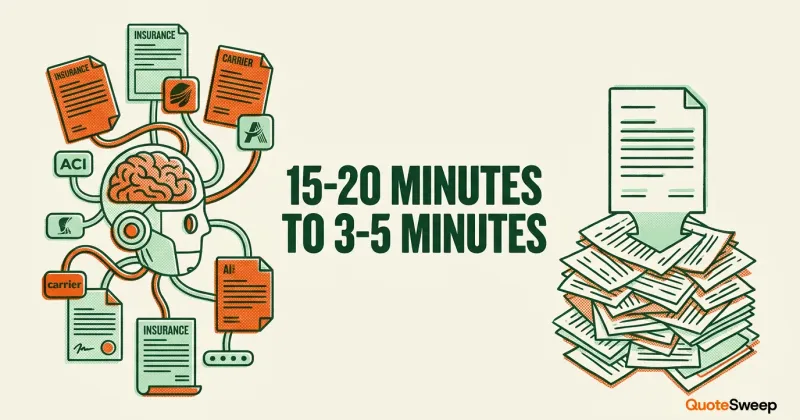

Real time savings: A CSR who spends 15–20 minutes per account manually entering data from existing documents can reduce that to 3–5 minutes with AI extraction and review. Across 10 accounts per day, that is 2+ hours recovered.

Appetite Matching and Carrier Selection

Carrier appetite – which carriers will write which classes of business in which states at what terms – has traditionally been tribal knowledge. An experienced agent knows that Carrier A likes restaurants but not bars, Carrier B writes contractors in Ohio but not California, and Carrier C will quote anything under $50K in premium but declines larger accounts. That knowledge lives in people's heads, not in systems.

What it does: AI-based appetite checking uses historical quoting data, carrier guidelines, class code analysis, and risk characteristics to predict which carriers on your panel are likely to offer competitive quotes for a specific account. Instead of submitting to 15 carriers and waiting to find out which 9 will actually respond, appetite matching filters to those 9 carriers upfront.

How well it works: The accuracy depends on the data behind it. Tools with large quoting datasets – hundreds of thousands of submissions across diverse carriers – can predict appetite with meaningful accuracy. Tools working from static carrier guideline documents are less accurate because carrier appetite shifts frequently and documentation lags behind reality. No appetite tool is 100% accurate, but even 75% accuracy eliminates a lot of wasted submissions.

Where to find it: QuoteSweep, Tarmika, Semsee, and several carrier-specific platforms include appetite matching. Some operate as standalone appetite checkers; others integrate appetite matching into the quoting workflow so carrier selection happens automatically before submissions are sent.

Real time savings: Eliminating wasted submissions – sending to carriers that decline or non-renew – saves 5–10 minutes per carrier per account. Across an agency handling 20 new business accounts per week, that can add up to several hours of weekly time savings.

Intelligent Field Mapping

Every carrier portal asks for the same basic information – business name, address, NAICS code, revenue, employee count, payroll, loss history – but in different formats, different field names, different sequences, and different dropdown menus. Field mapping is the AI layer that translates a single set of client data into each carrier's specific format.

What it does: When you enter "IT Consulting" as the business type, field mapping knows to enter NAICS 541512 on one carrier's portal, select "Professional Services - Technology" from a dropdown on another, and enter SIC code 7371 on a third. It handles the contextual translation that simple one-to-one data mapping cannot.

How well it works: For common class codes and standard fields, mapping accuracy is high – above 95% for well-maintained mapping libraries. Edge cases (unusual class codes, carrier-specific subquestions, conditional fields that only appear for certain risk types) still require human intervention. The technology improves over time as more submissions generate more mapping data.

Where to find it: This capability is embedded in AI web agents tools and comparative raters. It is not typically sold as a standalone product – it is part of the quoting workflow. For more on how this works, see our guide to AI web agents for insurance.

Real time savings: Field mapping is the technology that makes quoting 10 carriers from a single data entry possible. Without it, you enter data once per carrier. With it, you enter data once, period. The time savings scale with the number of carriers you quote per account.

Communication Drafting

AI-generated text – powered by the same large language models behind ChatGPT and similar tools – can draft client communications: renewal notices, coverage summaries, proposal emails, follow-up messages, and marketing content.

What it does: Given context about a client (their business type, coverage, upcoming renewal, recent quote results), AI can draft a first pass of common communications. "Draft a renewal notice for a restaurant owner whose BOP is renewing with a 12% rate increase" produces a usable starting point that a CSR or producer edits and personalizes.

How well it works: The drafts are competent but generic. They save time on the blank-page problem – getting from nothing to a reasonable first draft – but they require human editing to add the personal touch, specific details, and tone that clients expect from their agent. Using AI-drafted communications without review is a client relationship risk.

Where to find it: Several AMS platforms and CRM tools have integrated AI drafting. Vertafore added AI-powered client communications to AMS360. Standalone tools like ChatGPT, Claude, and Microsoft Copilot can be used directly with insurance-specific prompts. Some agencies build prompt templates for common communication types.

Real time savings: A CSR who writes 15–20 emails per day can save 1–2 minutes per email with AI-drafted starting points. That is 20–40 minutes per day – meaningful but not transformative.

AI That Is Getting Close but Not Quite There

These applications are in development, being tested by early adopters, and improving rapidly – but are not yet reliable enough for most agencies to depend on.

Policy Checking and Coverage Analysis

AI tools that compare policy language against client needs, flag coverage gaps, identify missing endorsements, and verify that bound coverage matches what was quoted. This is a genuine use case with clear value – the problem is accuracy.

Why it is not ready yet: Insurance policy language is dense, nuanced, and varies significantly across carriers. An AI that correctly identifies a coverage gap 85% of the time also misses one 15% of the time – and in insurance, missing a coverage gap creates E&O exposure. Most agencies are not comfortable with error rates that high for coverage analysis. The tools are improving, and the human-review-plus-AI-first-pass model works for some agencies, but fully automated policy checking is not yet trustworthy.

Predictive Lead Scoring

AI that analyzes prospect data – business characteristics, online behavior, industry trends – to predict which leads are most likely to bind. The concept is sound: focus producer time on high-probability prospects rather than treating every lead equally.

Why it is not ready yet: Predictive lead scoring requires large, clean datasets of historical lead-to-bind conversions. Most independent agencies do not have that data in a structured, analyzable format. The agencies that do – typically large brokerages with sophisticated CRM implementations – are seeing early value. For a 10-person agency with lead data scattered across spreadsheets, email inboxes, and memory, predictive scoring does not have enough data to work with.

Automated Submission Narratives

AI that generates the risk narrative portion of a submission – the written description of the account, the risk mitigation measures, the business context that underwriters want to see alongside the data. Good narratives improve quoting outcomes; generic ones hurt them.

Why it is not ready yet: The narratives AI generates are competent but formulaic. Underwriters read hundreds of submissions. An obviously AI-generated narrative that reads like every other AI-generated narrative does not help differentiate your submission. Experienced agents write narratives that highlight the specific strengths of an account in language that resonates with the specific carrier's underwriting philosophy. AI is not there yet for this type of nuanced, relationship-aware writing.

AI That Is Overhyped for Agencies

These are the use cases that conference speakers and vendor marketing materials promote heavily but that deliver little practical value for typical independent agencies today.

"AI-Powered Quoting"

No AI generates insurance quotes. Carriers generate quotes based on their actuarially filed rates, underwriting models, and risk assessment. When a vendor says "AI-powered quoting," they mean AI assists with data entry, field mapping, or carrier selection during the quoting process. The quote itself comes from the carrier.

This distinction matters because "AI quoting" sets an expectation that an agent enters minimal data and AI produces a bindable quote. That is not how commercial insurance works, and it is not how any tool works. For a deeper analysis, see our AI insurance quoting reality check.

Chatbots for Commercial Lines

Chatbots work for simple, transactional interactions: "What is my deductible?" or "Can you send me a certificate?" For commercial lines, where client conversations involve coverage analysis, risk assessment, and advisory judgment, chatbots are not useful. A business owner calling about their general liability limit after receiving a contract requirement does not want to talk to a chatbot.

Some agencies have deployed chatbots for after-hours basic service requests – and that is a reasonable use case. But chatbots replacing commercial lines conversations? Not happening.

Autonomous Agents (AI That Runs Your Agency)

The idea that an AI system could handle the end-to-end workflow of a commercial insurance placement – from initial prospect call to risk assessment to carrier selection to submission to negotiation to binding – is entirely theoretical. Each step involves judgment, relationship context, and domain expertise that current AI cannot reliably replicate. This is a 5–10 year vision at best, not a current capability.

How to Evaluate AI Tools for Your Agency

Ask What the AI Actually Does

When a vendor says their product "uses AI," ask specifically: What data does the AI process? What output does it produce? How accurate is it? What happens when it is wrong? The answers will tell you whether the AI is doing meaningful work (document extraction, field mapping) or whether "AI" is a marketing label on a simple rule-based system.

Demand Accuracy Numbers

Any AI tool making decisions or producing outputs that affect your workflow should have measurable accuracy. Document extraction tools should tell you their accuracy rate on different document types. Appetite matching should have hit-rate data. If a vendor cannot provide accuracy metrics, the AI is probably not mature enough to depend on.

Calculate the Real ROI

AI tool ROI for independent agencies comes from time savings, not from revenue generation. A tool that saves each of your 5 CSRs 90 minutes per day has a clear, measurable value. A tool that promises to "transform your client experience" does not. Focus on the specific tasks the AI automates, how much time those tasks currently take, and how much time they will take with AI assistance.

Start With the Bottleneck

The highest-ROI AI investment for most agencies is in whichever repetitive task consumes the most staff time. For most agencies, that is commercial quoting – entering the same data into multiple carrier portals. Before investing in AI-powered communication tools or predictive analytics, address the quoting bottleneck first. The time savings are larger and more immediate.

What the Next 2–3 Years Look Like

AI in insurance agencies is not standing still. Here is what is realistic to expect through 2028 based on current development trajectories.

Document Understanding Gets Better

AI will move from extracting data from standard form formats to understanding unstructured insurance documents – endorsements, policy language, exclusion schedules, coverage opinions. This will make policy checking and coverage analysis tools reliable enough for production use with human review.

Carrier API Adoption Grows (Slowly)

More carriers will expose APIs for commercial quoting, partially driven by AI tools that can interact with APIs more efficiently than with portals. But the 98% of carriers without APIs will not become 50% anytime soon. AI web agents will remain essential.

AMS and CRM Platforms Embed AI

Rather than buying standalone AI tools, agents will increasingly find AI features built into the platforms they already use. AMS platforms will add document extraction, communication drafting, and task prioritization. CRM platforms will add lead scoring and follow-up optimization. The buying decision shifts from "which AI tool?" to "which platform has the best embedded AI?"

Small Agencies Get Access

Today, the most sophisticated AI tools are priced for and adopted by large brokerages. Over the next 2–3 years, as AI development costs decrease and more tools embed AI into existing workflows, small agencies will gain access to capabilities that were previously available only to large operations. This democratization of AI tools is the most impactful trend for independent agents.

Frequently Asked Questions

Should my agency be using AI right now?

If "using AI" means buying standalone AI products and building AI workflows from scratch – probably not, unless you are a large agency with technical staff. If "using AI" means choosing quoting tools, AMS platforms, and CRM systems that have embedded AI features (document extraction, field mapping, appetite matching) – absolutely. You are likely already using AI indirectly through your existing tools.

Will AI replace insurance agents?

No. AI handles repetitive data tasks. Insurance agents handle relationships, judgment, advocacy, and advice. These are fundamentally different types of work. AI makes agents more productive by eliminating the low-value tasks – which gives agents more time for the high-value work that clients pay them for. The agents most at risk are those whose entire value proposition is data entry speed – and those agents are already being replaced by technology, not by AI specifically.

How much should I budget for AI tools?

For most small to mid-size agencies, AI spending should be embedded in your existing tool costs rather than a separate budget line. Choose a comparative rater with good field mapping and appetite matching. Choose an AMS with document extraction. Choose a CRM with communication drafting. The marginal cost of AI features within these platforms is much lower than buying standalone AI tools. Budget $0 for standalone AI and focus on choosing platforms with strong embedded AI capabilities.

What about ChatGPT and similar tools?

General-purpose AI tools like ChatGPT and Claude are useful for insurance agencies – for drafting communications, summarizing documents, researching coverage questions, and generating marketing content. They are free or low-cost and require no implementation. The limitation is that they are not connected to your data, your AMS, or your carrier portals. They are productivity tools for individual tasks, not workflow automation. Use them as supplements to your insurance-specific tools, not as replacements.

Is AI a security risk for my client data?

Any tool that processes client data – AI or otherwise – should meet your agency's data security standards. Before using AI tools with client information, verify: Where is the data processed? Is it stored? Who has access? Is it used to train the AI model? Reputable insurance technology vendors provide clear answers to these questions. Avoid uploading sensitive client data to general-purpose AI tools that do not have enterprise security and data handling commitments.