98% of P&C Carriers Have No API – Here's Why That Matters for Your Agency

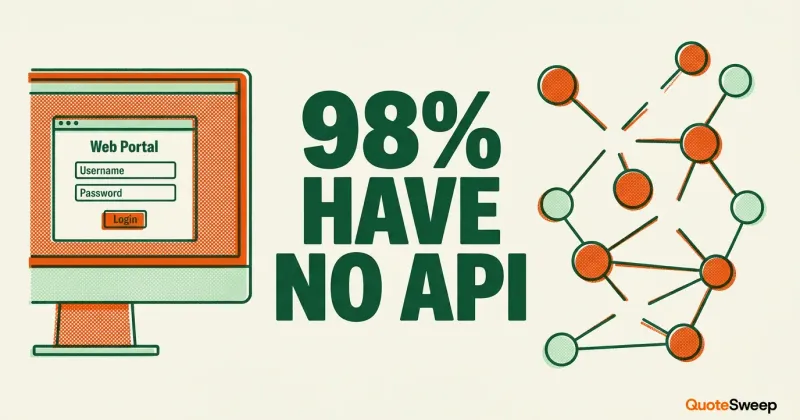

Of the roughly 2,700 property and casualty carriers operating in the United States, only about 60 are accessible through commercial quoting raters today – and when you drill into full BOP + GL + WC coverage, that number drops to roughly 8–10. That means approximately 98% of carriers can only be quoted by manually logging into their web portals, filling out forms, and waiting for results. This single fact explains more about the state of commercial insurance technology than any industry report or conference keynote.

The U.S. P&C market includes roughly 2,700 carriers. Herald's Insurance API Index counts 86 with any commercial API, but only ~8–10 offer full core commercial APIs (BOP + GL + WC) – the lines independent agents quote every day. Across rater platforms, roughly 50–60 unique carriers are reachable, leaving approximately 98% accessible only through manual portal login.

If you're an independent agent wondering why commercial quoting still feels stuck in 2005 while personal lines has been automated for a decade – the API gap is your answer.

Where the 98% Number Comes From

Let's break down the carrier landscape to show how we arrive at this figure.

The Total Carrier Count

According to NAIC regulatory filings and industry databases, there are approximately 2,700 property and casualty insurers operating in the United States. This includes national carriers (the household names like Travelers, Hartford, and Progressive), regional carriers (Erie in the Mid-Atlantic, Acuity in the Midwest, EMPLOYERS in workers' comp), specialty carriers, surplus lines markets, managing general agencies, and state-specific mutuals.

The P&C market is not a monolith dominated by a handful of companies. According to III data, the top 10 carriers write approximately 47–50% of total direct premiums – but the other half is spread across thousands of smaller carriers, many of which are the primary markets for independent agencies in their regions.

The API-Connected Carriers

The comparative raters that rely on API connections – platforms like Tarmika and Semsee – connect to approximately 31 to 48 carriers respectively. There's significant overlap between their carrier lists (the same major nationals appear on both), so the total number of unique carriers with commercial quoting APIs is roughly 50 to 60.

These are predominantly the large national carriers and a handful of larger regionals that have invested in building and maintaining API infrastructure: Travelers, CNA, Chubb, Liberty Mutual, Nationwide, Acuity, Hanover, Markel, MAPFRE, Westfield, and others in that tier.

The Math

Approximately 60 carriers with APIs out of roughly 2,700 total P&C carriers equals about 2.2% with API access – or roughly 98% without. This is an estimate based on publicly available carrier panel data from comparative rater platforms and total carrier counts from industry databases. The exact number shifts as carriers occasionally add API capabilities, but the ratio has remained remarkably stable over the past several years.

Why Most Carriers Don't Have APIs

It's easy to assume that carriers without APIs are simply behind the times. The reality is more nuanced. For most carriers, the business case for building a commercial quoting API doesn't pencil out.

The Cost of Building Insurance APIs

A commercial insurance API isn't a weekend project. It requires:

-

Integration with the policy administration system. Most regional carriers run on legacy platforms – Guidewire, Majesco, Duck Creek, or custom-built systems from the 1990s and 2000s. Exposing rating logic through a modern API means building an abstraction layer on top of these systems.

-

Maintaining the API as underwriting rules change. Carrier appetite, class codes, state eligibility, and pricing factors change constantly. Every change needs to be reflected in the API, tested, and deployed without breaking existing integrations.

-

Security and compliance. Insurance data includes personally identifiable information, business financial data, and loss history. An API must meet security standards, handle authentication, rate-limit requests, and maintain audit trails.

-

Developer support. Once you publish an API, integration partners need documentation, sandbox environments, technical support, and versioning. This is an ongoing operational cost.

For a carrier writing $5 billion in annual premium with dedicated engineering teams, this investment makes sense. For a regional mutual writing $100 million in premium with a 10-person IT department already stretched thin maintaining the existing policy admin system – it doesn't.

Legacy Technology Constraints

Many regional carriers operate on policy administration systems that were designed decades ago. These systems work well for their intended purpose – processing policies, managing claims, handling billing – but they were never architected for external API access.

Retrofitting an API onto a legacy system is expensive and risky. It often requires changes to core business logic, database schemas, and security infrastructure. For carriers that are already planning a multi-year platform modernization, adding an API is a "someday" item, not a current priority.

The Volume Equation

Large national carriers process millions of quotes annually. At that volume, API efficiency delivers meaningful operational savings. A regional carrier processing tens of thousands of quotes – many of which come through established agency relationships rather than third-party platforms – sees less compelling returns.

When an agent is appointed with a regional carrier, they typically have a direct relationship with underwriters. The agent calls, emails, or logs into the carrier's portal. The carrier's portal works fine for their existing distribution channel. An API would serve the comparative rater platforms, but the carrier has to weigh the development cost against the incremental business those platforms would generate.

Brand Equity: Some Carriers Refuse on Principle

Cost and legacy explain most of the API gap, but not all of it. Some large national carriers have the budget and the engineering capacity to ship an API. They've chosen not to.

The reason that comes up repeatedly in conversations with agency owners and franchise brokerage executives: brand equity. A national carrier worries that exposing itself through a comparative rater puts it in a side-by-side column with cheaper or hungrier competitors. What was a brand-driven distribution relationship (agents calling the underwriter, agents knowing the appetite) becomes a price-shopping exercise. The carrier loses the touchpoint where it can differentiate beyond price.

Hartford is the canonical example. According to multiple agency leaders we've spoken with, including the leadership of one franchise brokerage that pitched Hartford repeatedly over several years, Hartford has declined to expose its small commercial BOP API to third-party raters. Not on technical grounds. The reason given was positioning: Hartford's small commercial book moves through agent relationships and direct portal logins, and Hartford prefers that distribution surface over a rater column where price is the deciding factor.

This is rational from the carrier's side. It's also why "wait for more APIs" isn't a strategy for agents. Some of the carriers you care most about may never participate, no matter how mature the rater landscape gets.

What This Means for Independent Agents

The API gap isn't an abstract technology problem. It directly affects how independent agents run their businesses every day.

Your Best Markets May Be Unreachable by API Tools

According to the 2024 Big I Agency Universe Study, independent agencies are appointed with an average of 17 carriers. For many agencies – particularly those outside major metro markets – a significant portion of those appointments are regional carriers. Erie in Pennsylvania, Acuity in Wisconsin, Cincinnati Financial in the Midwest, Donegal in the Mid-Atlantic, West Bend Mutual in the upper Midwest.

These regional carriers often offer advantages that nationals don't: higher commissions, more flexible underwriting, deeper local relationships, and willingness to write risks that nationals decline. They're some of the best markets in an agent's panel.

But if your quoting tool can only reach carriers with APIs, your regional appointments are left out. You're still manually quoting those carriers – which means you're either spending the time to log into their portals individually, or you're not quoting them at all and leaving money on the table.

The Time Tax Is Real

An agent who quotes 10 carriers manually for a commercial account spends 60 to 90 minutes on data entry. If 4 of those carriers are accessible through an API-based comparative rater, the rater saves time on those 4 – but the agent still has to manually quote the other 6. The time savings from a partial solution are real but limited.

The agent who quotes 10 carriers through a tool that can access all 10 – regardless of API availability – eliminates the manual work entirely. That's the difference between a 30% time reduction and a 90% time reduction.

State-Specific Markets Amplify the Problem

Some states are dominated by carriers that don't have API connections. In the upper Midwest, carriers like West Bend, SECURA, and Society Insurance are major commercial writers but aren't available through API-based comparative raters. In the Northeast, many mutual carriers operate the same way. In specialty workers' comp markets, carriers like EMPLOYERS and Key Risk focus on specific niches and haven't built broad API integrations.

If you're an agent in these markets, API-based tools cover only a fraction of your carrier panel.

AI Web Agents: Bridging the API Gap

If most carriers aren't going to build APIs anytime soon, the practical question becomes: how do you automate quoting with carriers that only have web portals?

The answer is AI web agents.

How It Works

AI web agents interacts with carrier web portals the same way an agent would – logging in, navigating to the quoting workflow, filling out forms, submitting applications, and extracting results. But instead of doing this one carrier at a time, it does it across multiple carriers simultaneously.

Think of it as a very fast, very accurate assistant who can log into 15 carrier portals at the same time, enter your client's information into each one, and bring back all the quotes. The assistant uses the carrier's own portal – no API required – so it works with any carrier that has a web-based quoting workflow.

This is the approach QuoteSweep takes. Because it doesn't depend on carrier API partnerships, it can reach the roughly 98% of carriers that API-only tools cannot.

Why Not Just Build More APIs?

This is the question carriers, industry groups, and InsurTech companies ask constantly. Organizations like IVANS and ACORD are pushing for standardized data exchange, and some progress is being made. But the adoption curve is long.

Consider: most of the carriers that have APIs today built them years ago. The carriers that haven't built APIs by now are unlikely to in the next two to three years, given the cost, complexity, and competing priorities. And even when a carrier does launch an API, it takes time for comparative rater platforms to integrate with it, test it, and make it available to agents.

AI web agents isn't a stopgap. It's the pragmatic solution for the market as it actually exists today – and for the foreseeable future.

Limitations to Acknowledge

AI web agents isn't perfect. It depends on carrier portals being available and functioning normally. When a carrier redesigns its portal, the automation needs to adapt. Internet connectivity and portal speed affect performance. These are real operational considerations that don't apply to API-based quoting.

That said, for the vast majority of quoting scenarios, AI web agents delivers results reliably and quickly – and it works with carriers that agents would otherwise have to quote entirely by hand.

The Future: Will the API Gap Close?

Slowly. Some trends are pushing in the right direction:

-

Platform modernization. As carriers replace legacy policy admin systems with modern platforms (Guidewire Cloud, Duck Creek OnDemand), API capability becomes easier to add. But these migrations take years.

-

Industry standards. ACORD's data standards and IVANS' connectivity platform are reducing the friction of building carrier integrations. But standards adoption is gradual, not instantaneous.

-

Competitive pressure. As more agents use comparative raters, carriers that aren't accessible through these tools may lose submission volume. This creates an incentive to build API access – eventually.

The realistic outlook: the number of carriers with APIs will grow from 50 to perhaps 75 or 100 over the next several years. That's meaningful progress. But even at 100 carriers with APIs, over 95% of the market would still be API-free. The long tail of regional, specialty, and niche carriers will remain portal-only for the foreseeable future.

For agents, the practical takeaway is clear: don't wait for the industry to solve the API problem. Use tools that work with the carrier landscape as it exists today. Your carrier panel includes carriers without APIs, and your quoting workflow should be able to reach all of them.

For a comparison of tools that take different approaches to this problem – API-only vs hybrid vs AI web agents – see our Tarmika vs Semsee vs QuoteSweep comparison.

Frequently Asked Questions

Where does the 2,700 carrier number come from?

NAIC regulatory filings and industry databases track the total number of licensed property and casualty insurers in the United States. The exact count varies by source (some include all licensed entities, others focus on active writers), but the figure consistently falls in the 2,500 to 2,800 range.

Which carriers DO have APIs for commercial quoting?

The carriers accessible through API-based comparative raters include Travelers, CNA, Chubb, Liberty Mutual, Nationwide, Acuity, Hanover, Markel, MAPFRE, Westfield, Employers, AmTrust, and approximately 25 to 30 others. These tend to be the larger national and regional carriers.

Is AI web agents secure?

Yes – when implemented correctly. AI web agents uses the agent's own carrier portal credentials, encrypted in transit and at rest. The automation accesses carrier portals through the same secure connection an agent would use manually. QuoteSweep maintains enterprise-grade security practices for credential storage and portal interaction.

Will IVANS or ACORD solve the API gap?

They're working on it, and progress is real. But standardization and adoption take time. Even optimistic projections suggest the majority of carriers will remain portal-only for at least several more years.