EPLI Insurance: What Agents Need to Know

Employment Practices Liability Insurance – EPLI – covers businesses against claims brought by employees (or former employees, applicants, and sometimes third parties) alleging wrongful employment practices. These claims include wrongful termination, discrimination, harassment, retaliation, and wage-and-hour disputes. For agents, EPLI is a line that should be part of every commercial account conversation, because the exposure is universal: every business with employees faces employment practices risk, and the costs of defending even a baseless claim can be devastating.

The numbers back this up. According to the EEOC, there were over 88,500 charges of workplace discrimination filed in fiscal year 2024. That figure only captures federal EEOC filings – it doesn't include state-level agency complaints, private lawsuits, or demand letters that never become formal charges. The true volume of employment-related claims is far higher, and businesses of all sizes are targets.

EPLI fits naturally alongside other management liability lines like D&O and fiduciary liability. Unlike general liability insurance, which covers bodily injury and property damage to third parties, EPLI addresses a fundamentally different exposure – allegations arising from the employment relationship itself.

TLDR: EPLI covers businesses against lawsuits alleging wrongful employment practices – discrimination, harassment, wrongful termination, retaliation, and related claims. Virtually every business with employees faces this exposure. Policies are written on a claims-made basis, with premiums ranging from $800 to $5,000+ annually for small businesses depending on size, industry, and claims history. Defense costs alone average $75,000 to $125,000 per claim, making EPLI essential even for businesses with strong HR practices.

What EPLI Covers

EPLI policies cover the insured organization (and typically its directors, officers, and managers as individual insureds) against claims alleging wrongful employment practices. The core covered acts include:

Wrongful Termination

The single most common EPLI claim type. An employee alleges they were fired for an illegal reason – discrimination based on a protected characteristic, retaliation for filing a complaint, breach of an implied employment contract, or violation of public policy. Even in at-will employment states, wrongful termination claims are common and expensive to defend.

Discrimination

Claims that an employer made adverse employment decisions – hiring, firing, promotion, compensation, job assignment – based on a protected class. Federal protections under Title VII, the ADA, ADEA, and other statutes cover race, color, religion, sex (including pregnancy and sexual orientation), national origin, age (40+), disability, and genetic information. State and local laws often expand protected classes to include marital status, political affiliation, and other categories.

Sexual Harassment and Workplace Harassment

Claims of hostile work environment or quid pro quo harassment. Post-#MeToo, harassment claims have increased in both frequency and severity. EPLI covers defense costs and settlements/judgments arising from harassment allegations – whether the harasser is a supervisor, coworker, or in some policies, a customer or vendor.

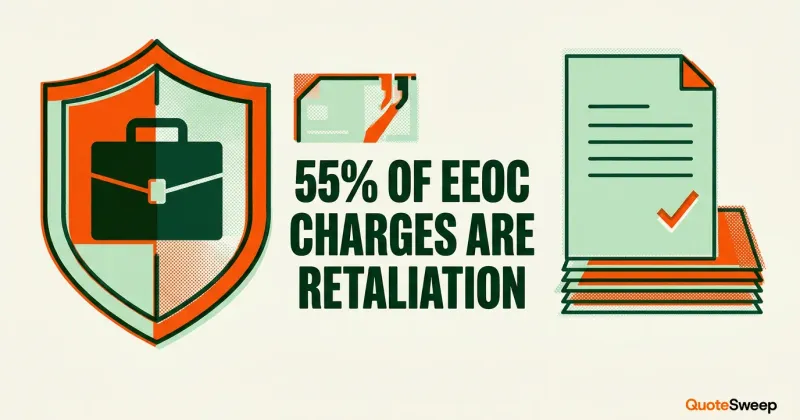

Retaliation

The fastest-growing category of employment claims. EEOC data shows retaliation charges have been the most frequently filed charge type since 2009, accounting for over 55% of all EEOC charges in recent years. Retaliation claims allege that the employer took adverse action against an employee who engaged in protected activity – filing a discrimination complaint, reporting safety violations, taking FMLA leave, or participating in an investigation.

Wage and Hour Claims

Coverage for wage and hour claims varies significantly by policy. Some EPLI forms include wage and hour as a covered employment practice; others exclude it entirely or offer it as an optional endorsement with a sublimit. Because class-action wage and hour claims can involve massive exposure (thousands of employees across multiple states), many carriers limit or exclude this coverage. When it is available, it's typically sublimited to $25,000–$100,000 in defense costs only, with no coverage for the underlying wage payments owed.

Additional Covered Claims

Depending on the policy form, EPLI may also cover:

- Failure to promote or hire – an applicant or employee alleges they were passed over based on a protected characteristic

- Negligent evaluation – an employee claims their performance review was conducted improperly, leading to demotion or termination

- Breach of employment contract – allegations that the employer violated the terms of a written or implied employment agreement

- Deprivation of career opportunity – claims that management decisions unfairly limited an employee's professional advancement

- Wrongful discipline – allegations that disciplinary actions were disproportionate or discriminatory

- Invasion of privacy – claims related to monitoring, searches, or inappropriate disclosure of employee information

- Emotional distress / mental anguish – arising from any of the above employment practices

Who Needs EPLI

Every Business with Employees

The short answer is: any business that employs people. The exposure exists whether the business has 3 employees or 3,000. In fact, smaller businesses are often more vulnerable because they lack formal HR departments, documented policies, and the internal processes that help prevent claims and support defenses.

Industries with Higher EPLI Exposure

Some industries face elevated employment practices risk:

| Industry | Key Risk Factors |

|---|---|

| Healthcare | High employee turnover, diverse workforce, patient-facing stress |

| Hospitality/restaurants | Tipping disputes, harassment in customer-facing roles, high turnover |

| Retail | High employee counts, wage and hour issues, seasonal staffing |

| Financial services | Compensation disputes, discrimination in promotion, regulatory scrutiny |

| Technology | Age discrimination, gender equity issues, non-compete disputes |

| Construction | Wage and hour violations, immigration-related claims, safety retaliation |

| Nonprofits | Volunteer vs. employee disputes, limited HR resources |

Businesses Going Through Transitions

Businesses that are downsizing, restructuring, merging, or going through leadership changes face heightened EPLI exposure. Layoffs and restructurings produce wrongful termination claims. Mergers bring culture clashes and redundancies. New management may inherit liability for prior employment practices they didn't even know about.

How EPLI Policies Are Structured

Claims-Made Coverage

EPLI is written on a claims-made basis, which means two conditions must be met for coverage to apply:

- The claim must be reported during the policy period

- The wrongful act must have occurred after the retroactive date

This means retroactive dates matter enormously when placing or remarketing EPLI. Moving a retroactive date forward creates a gap in coverage for prior acts – and prior acts are exactly where most EPLI claims originate, since employment disputes often stem from actions taken months or years before the claim is filed.

Defense Cost Provisions

EPLI policies handle defense costs in two ways:

- Duty to defend – the carrier selects defense counsel and manages the defense directly, similar to a CGL policy. Less common in EPLI.

- Duty to reimburse (also called "indemnity" or "non-duty-to-defend") – the insured selects counsel, manages their own defense, and submits costs to the carrier for reimbursement. This is the more common structure in EPLI.

Critical distinction: Most EPLI policies have defense costs inside the limit (also called "eroding limits" or "burning limits"). This means defense costs reduce the policy limit available for settlements or judgments. If a $1 million EPLI policy has $300,000 in defense costs, only $700,000 remains for a settlement or verdict. This is different from CGL, where defense costs are typically outside the limit.

Retention (Deductible)

EPLI retentions typically range from $2,500 to $25,000 for small businesses and can reach $50,000 to $250,000+ for mid-market and larger accounts. Some carriers apply the retention to defense costs and indemnity combined; others apply it only to indemnity. Understanding how the retention applies is important when comparing quotes.

EPLI Pricing Factors

EPLI premiums vary widely based on risk characteristics. For small businesses (under 50 employees), annual premiums typically fall in the $800 to $5,000 range. Mid-market accounts (50–500 employees) may pay $5,000 to $25,000+. Large accounts are individually rated.

Primary Rating Variables

- Number of employees – the most significant rating factor. More employees mean more potential claimants. Full-time, part-time, seasonal, and temporary employees are all counted.

- Industry/SIC or NAICS code – certain industries carry higher EPLI rates due to historical claim frequency. Hospitality, healthcare, and retail typically rate higher than professional services or manufacturing.

- Annual revenue – used as a secondary measure of business size and exposure

- Prior claims history – any history of employment-related claims, EEOC charges, or lawsuits significantly affects pricing. Even a single claim can increase premiums 25%–50%.

- Geographic location – states with plaintiff-friendly employment laws (California, New York, New Jersey, Illinois) carry higher rates than states with more employer-friendly legal environments

- HR practices – carriers often provide credits for businesses that have written employee handbooks, formal complaint procedures, documented termination processes, and regular management training

- Years in business – startups and newer businesses may face higher rates due to lack of established HR processes

- Employee turnover rate – high turnover correlates with higher claim frequency

Premium Benchmarks

| Business Size | Typical Annual Premium Range | Typical Limit |

|---|---|---|

| 1–10 employees | $800–$2,000 | $250K–$500K |

| 11–50 employees | $2,000–$5,000 | $500K–$1M |

| 51–200 employees | $5,000–$15,000 | $1M–$2M |

| 201–500 employees | $15,000–$30,000 | $2M–$5M |

These ranges are approximate and vary by industry, state, and claims history. Accounts with prior claims or in high-risk industries can significantly exceed these benchmarks.

Common EPLI Exclusions

Standard Exclusions

Most EPLI policies exclude:

- Criminal, fraudulent, or intentionally wrongful acts – once established by final adjudication. Note: the insurer still provides a defense until wrongful intent is proven. Some policies include a "final adjudication" standard; others use broader language.

- Bodily injury and property damage – these exposures are covered under general liability. However, some EPLI policies cover emotional distress arising from employment practices, even though emotional distress can be considered a type of "bodily injury" under GL.

- ERISA and employee benefits claims – disputes over retirement benefits, health insurance, and other employee benefit plans are excluded (covered under fiduciary liability policies)

- Workers' compensation claims – on-the-job injuries are covered by workers' comp, not EPLI

- WARN Act violations – the federal Worker Adjustment and Retraining Notification Act requires 60-day notice of mass layoffs. Violations are typically excluded from EPLI.

- OSHA penalties and fines – regulatory fines are generally uninsurable

- National Labor Relations Act (NLRA) proceedings – union organizing disputes and unfair labor practice charges are typically excluded

- Prior and pending litigation – claims or circumstances known before the policy inception date

- Wage and hour (in many forms) – as discussed above, many policies exclude or sublimit this coverage

Exclusions That Vary by Carrier

- Third-party claims – some EPLI policies cover claims by customers, vendors, or other non-employees alleging harassment or discrimination by the insured's employees. Others exclude third-party claims or offer them by endorsement. Third-party coverage is increasingly important for businesses with customer-facing operations.

- Punitive damages – coverage for punitive damages depends on state law (some states prohibit insuring punitive damages) and policy terms. Where allowed, some carriers include punitive damages; others exclude them.

EPLI Claims Examples

Understanding real-world claim scenarios helps agents explain EPLI's value to clients:

Wrongful Termination Claim

A 25-person accounting firm fires a 58-year-old senior accountant, citing performance issues. The employee sues alleging age discrimination, claiming younger employees with similar performance records were not terminated. Defense costs total $95,000 over 14 months. The case settles for $185,000 – a total claim of $280,000. Without EPLI, the firm pays this out of pocket.

Sexual Harassment Claim

A restaurant employee alleges that a manager made repeated unwelcome advances and that management failed to act on complaints. The employee files an EEOC charge and then sues. Defense costs reach $110,000. The jury awards $350,000 in compensatory damages. Total claim: $460,000.

Retaliation Claim

An employee at a manufacturing company reports safety violations to OSHA. Three months later, the employee is transferred to a less desirable shift. The employee sues alleging retaliation. Even though the employer argues the transfer was unrelated, defending the claim costs $85,000 before settling for $125,000. Total: $210,000.

Failure to Promote

A female sales associate at a retail company is passed over for promotion three times in favor of male colleagues. She files a gender discrimination lawsuit. Defense costs: $70,000. The case settles for $150,000, plus the company agrees to implement promotion tracking procedures.

Key Takeaway from Claims Data

According to the Hiscox Guide to Employee Lawsuits, the average cost to defend and settle an employment claim was approximately $160,000 as of their most recent study. Even claims that are ultimately dismissed without payment cost an average of $75,000 in defense costs alone. For a small business, these amounts can be existential threats.

How to Quote EPLI

Information Needed

Before approaching carriers, gather the following:

- Employee count – full-time, part-time, seasonal, temporary, and independent contractors (some carriers count 1099 workers)

- Industry and operations description – SIC/NAICS code and a description of what the business does

- Annual revenue and payroll – secondary rating factors

- HR practices documentation – does the business have an employee handbook? Written policies on harassment, discrimination, and termination? Regular management training?

- Claims history – prior EEOC charges, state agency complaints, lawsuits, demand letters, or any circumstances that could give rise to a claim (5-year lookback minimum)

- Employee turnover data – voluntary and involuntary terminations over the past 2–3 years

- Geographic footprint – states where employees are located (multi-state operations face the employment laws of each state)

- Prior EPLI coverage – current carrier, limits, retention, retroactive date, premium

- Planned changes – upcoming layoffs, restructurings, mergers, or significant hiring

Carrier Considerations

EPLI is available from multiple sources:

- Package/BOP endorsement – many carriers offer EPLI as an endorsement to a BOP or commercial package. This is typically the most cost-effective option for small businesses, though limits and coverage breadth are often more limited than standalone forms.

- Management liability package – EPLI bundled with D&O and fiduciary liability in a single policy. Common for mid-market accounts and often produces better combined pricing than standalone policies.

- Standalone EPLI – monoline EPLI for businesses needing higher limits, broader coverage, or specific endorsements not available on package forms.

- Surplus lines – accounts with prior claims, high-risk industries, or large employee counts may need surplus lines placement through an E&S market.

Quoting Tips

- Always compare defense cost treatment. Inside-the-limit vs. outside-the-limit defense costs is a meaningful coverage difference. A $1 million policy with defense inside limits provides significantly less protection than one with defense outside limits.

- Check retroactive dates carefully. When remarketing, ensure the new carrier matches the existing retroactive date. Moving it forward creates a coverage gap for prior employment acts – the most dangerous kind of gap for EPLI.

- Ask about wage and hour. If the client has wage and hour exposure (and most do), find out whether the policy covers it, excludes it, or offers it as an endorsement. This is a differentiator between carriers.

- Recommend third-party coverage. For businesses with customer-facing employees, third-party EPLI coverage is important. A customer who alleges harassment by an employee can sue the business – and CGL typically doesn't cover it.

- Factor in the underwriting appetite. Some carriers won't write EPLI for certain industries (staffing firms, nightclubs, adult entertainment). Know your carriers' appetite before quoting.

Risk Management: Reducing EPLI Exposure

Part of the value agents provide is helping clients reduce their employment practices risk. Carriers reward these practices with premium credits, and clients benefit from fewer claims:

Essential HR Practices

- Written employee handbook – clearly stating policies on harassment, discrimination, termination, compensation, and complaint procedures. Updated annually.

- Consistent documentation – every hiring decision, performance review, disciplinary action, and termination should be documented with specific, objective reasons.

- Regular management training – supervisors and managers should receive annual training on harassment prevention, proper documentation, and lawful employment practices.

- Complaint and investigation procedures – a clear process for employees to report concerns, with documented investigations and follow-up.

- Exit interviews – identify potential claims before they become formal disputes.

Common Triggers to Watch

Help clients understand the situations most likely to produce claims:

- Terminating employees who recently filed complaints, took FMLA leave, or reported safety issues (retaliation exposure)

- Layoffs that disproportionately affect employees of a particular age, race, or gender

- Inconsistent application of policies (one employee is fired for lateness while another is counseled)

- Failure to address reported harassment or inappropriate behavior

- Making employment decisions based on subjective criteria without documentation

Frequently Asked Questions

How much does EPLI cost for a small business?

For businesses with under 50 employees, EPLI premiums typically range from $800 to $5,000 annually, depending on industry, location, employee count, and claims history. The most cost-effective option for small businesses is often an EPLI endorsement on a BOP or commercial package rather than a standalone policy.

Does general liability cover employment claims?

No. General liability covers bodily injury and property damage claims from third parties – customers, visitors, and the public. Employment-related claims (wrongful termination, discrimination, harassment) are specifically excluded from CGL policies. EPLI is the coverage designed for these exposures.

Do small businesses really get sued by employees?

Yes. EEOC data shows that businesses of all sizes face employment discrimination charges. Small businesses are often more vulnerable because they lack dedicated HR staff, formal policies, and documentation practices. A single employment lawsuit can cost $100,000 or more in defense costs alone – an amount that can threaten the survival of a small business.

What is the difference between EPLI and D&O insurance?

EPLI covers claims arising from employment practices – how the business treats its employees. D&O (Directors & Officers) insurance covers claims arising from management decisions that affect the company, its shareholders, or third parties – allegations of mismanagement, breach of fiduciary duty, or regulatory violations. There is some overlap (a discrimination claim against a director could trigger either policy), which is why EPLI and D&O are often bundled in a management liability package.

Is EPLI claims-made or occurrence?

EPLI is almost always written on a claims-made basis. This means the claim must be reported during the policy period, and the alleged wrongful act must have occurred after the policy's retroactive date. If a claims-made EPLI policy is canceled without purchasing tail (extended reporting) coverage, the insured loses the ability to report claims for prior employment acts.

Shopping EPLI for your business

Most EPLI is placed through an agent, often bundled with D&O in a management-liability package. Businesses comparing the market directly can also work with a specialty brokerage. One AI-native option that lists employment practices liability among the coverages it places is Panta.