Cross-Selling Commercial Lines: Agent's Guide

Here's a number that should keep every agency owner up at night: 61% of policyholders have only one policy with their agent. That's more than half your book of business sitting on a single policy – the thinnest possible relationship, and the most vulnerable to a competitor's quote.

The flip side is just as compelling. Selling to an existing customer is 60–70% profitable compared to 5–20% for new prospects, and it costs 3 to 5 times less than acquiring a new client. Cross-selling isn't just a revenue strategy. It's a retention strategy, an efficiency strategy, and the fastest path to a more valuable book.

This guide covers how to identify cross-sell opportunities in your existing accounts, which lines pair best together, when to make the approach, what to say, and how to measure your progress.

TLDR: Most agents have massive untapped revenue sitting in their existing book. The key to cross-selling commercial lines is systematic account review, timing your approach around renewals and life events, and using specific scripts that connect coverage gaps to business risks – not generic "have you thought about" pitches.

Why Cross-Selling Beats New Business Acquisition

We're not saying to stop prospecting for new accounts. But if you're spending 100% of your sales energy on new business and 0% on account rounding, your economics are backwards.

The Math on Existing Clients vs. New Prospects

| Factor | New Prospect | Existing Client |

|---|---|---|

| Cost to acquire | 5x higher | 1x (baseline) |

| Close rate | 15–25% | 40–60% |

| Time to close | 4–8 weeks avg | 1–2 weeks avg |

| Retention rate (year 1) | 75–80% | 90%+ with 2+ policies |

| Revenue per interaction | Single policy | Multiple policies |

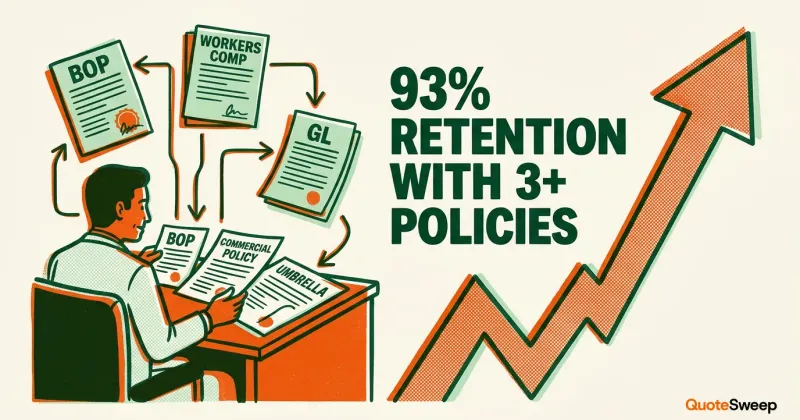

The retention stat is the most important. A client with one policy renews at roughly 80%. A client with three policies renews at 93% or higher. Every policy you add to an account makes the entire relationship stickier.

Account Rounding and Book Value

Agency valuations are driven by revenue, retention, and revenue per account. An agency with 1,000 accounts averaging 1.2 policies each is worth significantly less than an agency with 1,000 accounts averaging 2.4 policies each – even at the same total premium volume – because the higher-density book will retain better and cost less to service.

If you're thinking about building equity in your book, cross-selling is the most capital-efficient way to do it.

Identifying Cross-Sell Opportunities in Your Existing Book

Cross-selling starts with data, not gut feel. Before you pick up the phone, you need to know which clients have gaps and which gaps are the biggest opportunities.

The Account Audit Process

Run a report from your agency management system that shows every client, their active policies, and their industry classification. Then build a gap matrix:

Step 1: List expected lines by industry. A contractor should have GL, WC, commercial auto, inland marine, umbrella, and possibly builder's risk. A restaurant needs a BOP, liquor liability, WC, umbrella, and EPLI once they hit a certain employee count.

Step 2: Compare expected vs. actual. Flag every account where the client has fewer lines than their industry typically requires.

Step 3: Prioritize by revenue potential. A contractor with GL but no WC, auto, or umbrella represents $8,000 to $15,000 in additional premium. A retailer missing only a small crime endorsement represents $300. Prioritize accordingly.

Step 4: Check carrier appetite. Before you call, confirm that your existing markets can write the additional lines. The easiest cross-sell is one where the same carrier can add the coverage – it simplifies billing, reduces the client's admin burden, and often qualifies for a multi-policy discount.

Signals That Trigger Cross-Sell Conversations

Beyond the static gap analysis, watch for dynamic triggers:

- Renewal coming up in 60 days – The most natural time to discuss additional coverage

- New employees added – Triggers WC review, EPLI discussion

- New location or vehicle – Property, auto, and inland marine opportunities

- Claim filed – After a claim is resolved, the client is primed to discuss better protection

- Industry regulatory change – New compliance requirements can create coverage needs

- Client mentions growth plans – Expansion means new exposure

- Certificate request for higher limits – They need more coverage than they currently carry

Which Lines Cross-Sell Best Together

Not all cross-sell combinations perform equally. Some are natural extensions that make immediate sense to the client. Others require more education. Here's what we see working most consistently:

High-Conversion Combinations

BOP to Workers' Compensation If a client has a BOP but no WC, they have employees who are unprotected. In most states, WC is mandatory once you hit the employee threshold (often 1 to 5 employees depending on the state). This is a compliance conversation, not a sales pitch.

Conversion rate: Very high. It's legally required.

General Liability to Umbrella Clients with CGL often carry minimum limits because that's what they were quoted. An umbrella is inexpensive relative to the additional protection – often $500 to $1,500 annually for $1 million in additional limits. When a client's customer requires higher certificate limits, this is an easy close.

Conversion rate: High, especially for contractors and service businesses.

Property to Inland Marine Business owners who insure their building and contents often forget about equipment that leaves the premises. Contractors, caterers, photographers, and mobile service businesses all have tools and equipment that property policies exclude once they're off-premises.

Conversion rate: Moderate to high for applicable industries.

BOP to Cyber Liability With 35% of small businesses lacking cyber insurance and data breaches affecting businesses of all sizes, cyber is the fastest-growing cross-sell opportunity in commercial lines. Any client processing credit cards, storing customer data, or operating a website has exposure.

Conversion rate: Moderate and rising as awareness increases.

GL + WC to Commercial Auto If a client has employees and general liability, ask if any employees drive for business purposes. Personal auto policies exclude business use. A single accident in an employee's personal vehicle on a work errand creates an uninsured exposure that the client doesn't know about.

Conversion rate: High once the exposure is explained.

The Account Rounding Ladder

Think of cross-selling as climbing a ladder for each account:

- First policy – Whatever line brought them in (usually BOP or GL)

- Second policy – The most obvious gap (usually WC or umbrella)

- Third policy – Industry-specific need (cyber, inland marine, E&O)

- Fourth+ policies – Specialized coverages (EPLI, D&O, crime, commercial auto)

Aim to move every account up at least one rung per year.

Timing: When to Make the Cross-Sell Approach

Timing is the difference between a cross-sell that feels helpful and one that feels like a sales push.

The Best Windows

60 to 90 days before renewal: You're already reviewing the account. Adding a coverage review to the renewal conversation is natural and expected.

Immediately after a claim: The client just experienced a loss and is emotionally aware of risk. If the claim revealed a gap – or if the claim could have been covered better – this is the moment to address adjacent exposures.

After a positive service interaction: The client just had a good experience with your agency (fast certificate, helpful answer to a question, smooth endorsement). Goodwill is high. Ask about the gap you've identified.

When the client reports a business change: New employees, new equipment, new location, new revenue stream. Every change creates new exposure. Your job is to connect the dots.

During annual coverage reviews: If you build a systematic annual review process (more on that in our coverage reviews guide), every review naturally surfaces cross-sell opportunities.

The Wrong Times

- During a claims dispute – Resolve the issue first

- Immediately after a rate increase – Give them time to adjust

- When the client has expressed frustration – Fix the relationship before selling more

- Monday mornings and Friday afternoons – Low receptivity for non-urgent conversations

Scripts and Conversation Starters That Work

Generic approaches ("Have you thought about cyber insurance?") get generic responses ("Not really, I'm good"). Specific, risk-based conversation starters get engagement.

The Gap-Based Opener

"[Client name], I was reviewing your account ahead of your renewal and noticed something I wanted to flag. You have solid GL and property coverage, but I don't see an umbrella policy on file. For a business doing the kind of contract work you do, most of your clients are going to start requiring $2 million in total limits on certificates. Right now you're at $1 million. Can we spend five minutes talking about what an umbrella would look like? It's usually a few hundred dollars for an extra million in protection."

The Trigger-Based Opener

"You mentioned last week that you hired three new employees. Congratulations – that's great growth. I want to make sure your coverage kept up with the headcount. In [state], once you have [threshold] employees, workers' comp is mandatory. Let's make sure you're squared away before it becomes a compliance issue."

The Claims-Based Opener

"I'm glad we got your claim resolved. One thing it highlighted is that your current limits are at the minimum for your class of business. If that claim had been $100,000 instead of $30,000, you'd have been out of pocket for the difference. I'd like to show you what a broader policy looks like – it's usually less than you'd expect."

The Certificate-Based Opener

"I got a certificate request from [general contractor / client's customer] asking for $2 million aggregate and $1 million per occurrence. Your current policy is at $1 million/$500,000. We have two options: we can increase your base limits, or we can add an umbrella that gives you a full extra million. The umbrella is usually cheaper. Want me to run both options so you can compare?"

The Industry News Opener

"I don't know if you saw this, but [industry association] just published data showing that [specific risk] claims in your industry are up [X]% this year. I wanted to make sure your coverage addresses that exposure. Can I run a quick review?"

Common Cross-Selling Mistakes

1. Selling What's Easy Instead of What's Needed

Agents sometimes push the line that's easiest to quote rather than the one the client actually needs. If a client needs EPLI but you don't have a good market for it, the temptation is to push cyber instead because you can quote it faster. Resist this. The client's gap is the starting point, not your product catalog.

2. Cross-Selling Without Data

Walking into a conversation without having reviewed the account first makes you look unprepared. Before every cross-sell conversation, pull the client's policy list, review their industry's typical coverage needs, and identify the specific gap you're addressing.

3. Pitching Too Many Lines at Once

You identified five gaps in an account. Don't dump all five on the client in one meeting. Start with the most critical gap, close it, then schedule follow-up for the next one. Overwhelming people with options creates decision paralysis.

4. Ignoring the Client's Current Financial Reality

A client who just absorbed a 15% rate increase on their BOP isn't ready to hear about adding $4,000 in new premiums. Read the room. Sometimes the right cross-sell timing is six months away, and pushing now damages the relationship for a long time.

5. Not Documenting the Conversation

Every cross-sell conversation should be documented in your management system – especially when the client declines coverage. This protects you from E&O claims ("My agent never told me I needed that") and creates a follow-up trigger for next year.

Measuring Cross-Sell Success

What gets measured improves. Track these metrics monthly:

Key Performance Indicators

| Metric | How to Calculate | Target |

|---|---|---|

| Policies per client | Total policies / Total clients | 2.0+ (aim for 2.5) |

| Single-policy accounts | Clients with 1 policy / Total clients | Below 40% |

| Cross-sell conversion rate | Cross-sells closed / Cross-sells attempted | 30%+ |

| Revenue per account | Total commission / Total accounts | Increasing quarter over quarter |

| Retention by policy count | Retention rate for 1-policy vs. 2+ policy clients | Track the gap |

Building a Cross-Sell Dashboard

Set up a simple monthly report that shows:

- Total accounts with identified gaps – your addressable cross-sell universe

- Accounts contacted this month – your activity level

- Cross-sells closed this month – your results

- Average new premium per cross-sell – your revenue impact

- Policies per client trend – your long-term progress

Review this dashboard in every team meeting. Celebrate wins. Diagnose what's not converting and why.

Technology Tools for Systematic Cross-Selling

Manual cross-selling depends on agent memory and motivation. Systematic cross-selling depends on workflows and automation.

What to Look For in Tools

- Gap identification reports – Your AMS should flag accounts missing expected lines for their industry

- Renewal pipeline with cross-sell triggers – 90-day advance notice of renewals with gap data attached

- Multi-carrier quoting – When you identify a cross-sell opportunity, you need to present competitive options fast

- Documentation and tracking – Every conversation logged, every declination recorded

- Automated touchpoints – Drip campaigns that educate clients about coverage gaps between your proactive outreach

The agents who treat cross-selling as a system rather than an occasional effort consistently outperform those who wing it.

Frequently Asked Questions

What's a realistic policies-per-client goal for a commercial book?

Industry benchmarks suggest that the top-performing agencies average 2.4 to 2.8 policies per commercial client. If you're currently at 1.3 to 1.5, set an intermediate target of 1.8 within 12 months. Research shows that reaching 1.8 policies per client reduces annual churn to roughly 5%, which represents 95% retention.

Should I discount the cross-sold policy to get the deal done?

Generally, no. The value proposition of adding a policy is convenience, coverage completeness, and the expertise you bring to the recommendation. If you start discounting cross-sells, you train clients to expect it. That said, many carriers offer multi-policy credits automatically – make sure you're presenting those built-in savings to the client. That's the carrier's discount, not yours.

How do I cross-sell when the client's existing policy is with a different carrier than what I'd recommend for the new line?

This is common and it's fine. Explain that different carriers specialize in different lines, and your job as an independent agent is to find the best fit for each coverage. Some clients actually appreciate knowing you're not locked into a single carrier. Over time, if one carrier proves to be best across multiple lines, you can consolidate at renewal.

What if my CSRs or producers push back on cross-selling because they're too busy with service work?

This is an operations problem, not a sales problem. If your team doesn't have time to cross-sell, they're spending too much time on tasks that should be automated or streamlined. Review your quoting workflow, service processes, and certificate issuance. The time you free up from efficiency improvements funds the time needed for cross-selling conversations.