How to Grow Your Insurance Agency Book Without Hiring Another Person

The math on growing an independent insurance agency usually leads to the same conclusion: hire more people. More CSRs to handle quoting. More producers to bring in accounts. More service staff to manage renewals. Headcount goes up, overhead goes up, and the margin between growth and profitability gets thin.

But the math changes when you remove the bottleneck. If the constraint on growth isn't the number of accounts available – it's the time it takes to quote each one – then expanding quoting capacity without adding staff changes everything. Here's how.

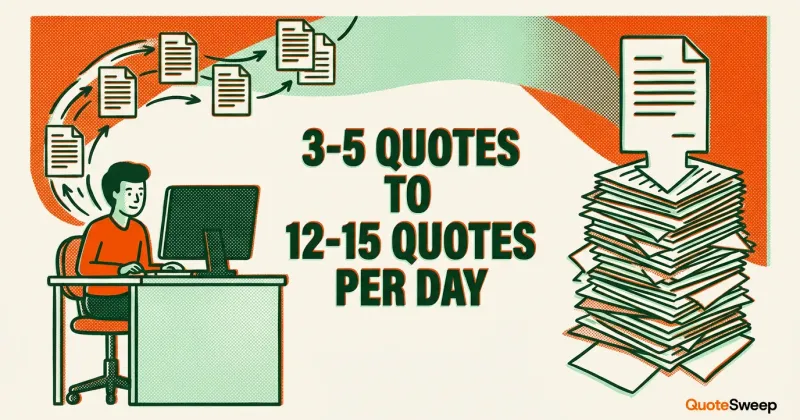

The bottleneck on agency growth usually isn't market opportunity – it's the time each quote takes. A comparative rater can double an agent's effective quoting capacity without adding staff: the same 5 accounts that took most of a day now take less than 30 minutes.

The Quoting Bottleneck Is Your Growth Constraint

Most independent agencies hit a ceiling that has nothing to do with market opportunity. There are plenty of accounts to quote. The problem is the time each quote takes.

The Manual Quoting Math

A CSR quoting commercial insurance manually follows a predictable workflow: gather client information, log into carrier portals one at a time, re-enter the same data into each carrier's forms, wait for quotes, compile results, and present to the client. For a single small commercial account quoted across 10 carriers, this takes 60 to 90 minutes.

An agent working a full day can handle 3 to 5 new commercial accounts using this manual process. Factor in service work, renewals, phone calls, and email, and many agents land closer to 3. That's the ceiling: 3 new commercial accounts per day, per agent, limited not by talent or effort but by the mechanics of re-keying data.

The Capacity Ceiling

At 3 accounts per day per agent, an agency with 3 CSRs handling commercial quoting can process approximately 9 new accounts daily or about 180 per month. If the agency needs to grow beyond that volume, the traditional answer is hire CSR number four. That means another $45,000 to $65,000 in annual salary plus benefits – before that person generates a dollar in new revenue.

The alternative: remove the quoting bottleneck so your existing 3 CSRs can each handle 10 to 15 accounts per day instead of 3. Your 180 monthly accounts become 600+ – without a single new hire.

How Quoting Automation Expands Capacity

A comparative rater replaces the manual portal-by-portal workflow with a single-entry, parallel quoting process. The agent enters client information once, the rater dispatches to all eligible carriers simultaneously, and quotes return in minutes instead of hours.

The time per account drops from 60 to 90 minutes to approximately 5 to 10 minutes. That's not incremental improvement – it's a 10x to 15x increase in quoting throughput.

Real Numbers

Say your agency has 2 commercial CSRs, each quoting 4 accounts per day manually. That's 8 accounts daily, roughly 160 per month.

With a comparative rater, each CSR can quote 12 to 15 accounts per day. That's 24 to 30 accounts daily, or 480 to 600 per month – from the same two people, in the same number of working hours.

The extra 320 to 440 accounts per month aren't theoretical. They're accounts your agency currently turns down, delays, or never pursues because there isn't time to quote them. They're the renewals you don't remarket because shopping 10 carriers takes too long. They're the prospects who went with another agency because you couldn't get quotes back fast enough.

The Revenue Math: What Extra Capacity Is Worth

Let's get specific with the numbers, because this is where agency owners either lean in or tune out.

Average Commercial Policy Economics

For a typical small commercial account:

- Average annual premium: $3,500

- Average agency commission rate: 12%

- Commission per new policy: $420

These are conservative midpoint figures. Larger accounts (contractors, manufacturers, multi-location businesses) generate significantly higher premiums and commissions. But the math works even at small commercial averages.

Scenario: Adding 5 Quotes Per Day

Assume quoting automation adds just 5 additional quoted accounts per day per agent – a conservative estimate given the 10x throughput improvement. With a 25% close rate on those additional quotes:

- Additional quotes per day: 5

- Additional policies won per day: 1.25 (at 25% close rate)

- Daily new commission: $525 (1.25 policies x $420)

- Monthly new commission: $10,500 (21 working days)

- Annual new commission: $126,000

That's from one agent adding 5 extra quotes per day. For an agency with 3 commercial CSRs, multiply accordingly.

The Renewal Compound Effect

New business commission is year-one revenue. But insurance policies renew. If you retain 85% of the new business you write (a reasonable retention rate for well-serviced commercial accounts), each year's new production compounds on the previous year's renewals.

After three years of adding $126,000 in annual new commission per agent:

- Year 1: $126,000 new commission

- Year 2: $126,000 new + $107,100 renewal (85% retention) = $233,100

- Year 3: $126,000 new + $198,135 renewal = $324,135

The book of business builds on itself. Automation doesn't just accelerate growth – it compounds it.

Five Growth Levers That Open With Automation

Quoting throughput is the foundation, but it enables several growth strategies that manual agencies can't practically execute.

1. Quote More Carriers Per Account

When quoting is manual, agents shortcut. Instead of quoting 12 carriers, they quote 4 or 5 – the ones they know best or the ones with the most convenient portals. This leaves competitive pricing on the table.

With automation, quoting 12 to 15 carriers takes the same time as quoting 3. More quotes means more competitive options. More competitive options means higher close rates. Studies consistently show that agents who present more carrier options win more accounts.

2. Remarket Every Renewal

Here's an industry truth that nobody likes to talk about: most agencies let commercial renewals auto-renew without shopping the market. Estimates from industry observers suggest the majority of commercial renewals go unmarketed. It's not laziness – it's time. Remarketing a renewal across 10 carriers takes the same 60 to 90 minutes as new business.

When remarketing takes 5 minutes, the calculus changes. An agency can systematically remarket every renewal 60 to 90 days before expiration, compare the renewal to fresh market quotes, and proactively reach out to clients with better options. This does three things:

- Protects retention by showing clients you're actively working for them

- Finds savings on accounts where the current carrier isn't competitive

- Generates referrals from clients impressed by proactive service

3. Respond Faster to Prospects

In a hard market, speed matters. When a business owner calls three agencies for quotes, the agency that responds first has a significant advantage. If your competitors are quoting manually and need 24 to 48 hours to compile options, and your agency can return quotes in 30 minutes, you're the one who earns the appointment.

Speed-to-quote is especially important for the accounts that come through online leads, association referrals, or your website's contact form. These prospects are shopping actively. The agency that gets back first with real quotes – not just "we'll review your account and get back to you" – wins disproportionately.

4. Use Appetite Checking to Avoid Wasted Effort

Not every carrier writes every risk. An IT consulting firm in Colorado has a different set of eligible carriers than a restaurant in Florida. Without appetite checking, agents submit to carriers that will decline – wasting time on both sides.

Automated appetite checking pre-filters your carrier panel before quoting. The agent sees instantly which carriers will consider the risk and which won't, based on class code, state, revenue, employee count, and other underwriting criteria. This means every submission goes to a carrier that's likely to quote – improving the ratio of quotes received to submissions sent.

5. Expand Into Adjacent Lines

When quoting your core lines (BOP, GL, workers' comp) takes less time, your agents have capacity to pursue cross-selling opportunities they currently don't have time for. That existing BOP client might need commercial auto. That GL account might be under-covered without an umbrella. The time freed by automating core quoting creates room to deepen relationships with existing clients – which is almost always the highest-ROI growth strategy.

How much new commission could your agency generate by expanding quoting capacity? Use the calculator below to see the math for your specific volume and time per account.

Calculate your ROI

At an average billing rate of $75/hr, that's

$27,500

in recovered capacity per year

If that time goes to closing 2-3 extra accounts per week at $500 avg commission

$50,000–75,000+

in additional annual revenue

Your QuoteSweep cost:

Pay As You Go: $4,000/yr

Team plan: $2,490/yr (annual)

How to Start: A Practical Roadmap

You don't need to overhaul your entire agency to capture these gains. Here's a phased approach.

Month 1: Automate New Business Quoting

Pick one comparative rater and deploy it for new commercial business. Don't try to change the renewal workflow, certificate process, or anything else simultaneously. Just replace the manual new business quoting workflow.

Measure the baseline first: how many accounts are your agents quoting per day right now? How long does each account take? Then measure after the first month with the new tool. The comparison will be stark enough to build momentum.

For help choosing the right tool, see our Tarmika vs Semsee vs QuoteSweep comparison or our insurance agency automation guide.

Month 2: Add Renewal Remarketing

Once your team is comfortable with the quoting tool for new business, extend it to renewals. Start with accounts renewing 60 to 90 days out that have rate increases of 10% or more – these are the accounts where remarketing is most likely to find better pricing and where clients are most motivated to see alternatives.

Build a weekly batch: every Monday, pull the renewals coming up in 60 to 90 days, filter for rate increases, and run them through the comparative rater. This becomes a systematic process rather than a reactive one.

Month 3: Optimize and Scale

By month 3, your team has the muscle memory. Now optimize: Which carriers are you winning with most often? Which risk classes are closing at the highest rates? Use this data to focus prospecting on the accounts where your carrier panel gives you the strongest competitive position.

This is also when the compound effect starts. The new business from Month 1 is settling. Renewals from Month 2 are retaining. Your book is growing while your headcount stays the same.

The Hiring Decision Changes, Not Disappears

Automation doesn't mean you'll never hire again. It means you hire for different reasons. Instead of hiring CSR number four because your existing three can't handle the quoting volume, you hire a producer because your agency's capacity can support more new business than your current producers can generate.

That's a fundamentally different hiring decision. Hiring to handle volume is defensive – you're running to keep up. Hiring to drive growth is offensive – you're investing in new revenue. Automation shifts you from the first to the second.

What This Looks Like in Practice

Consider a 5-person independent agency: the owner (who produces), 2 commercial CSRs, 1 personal lines CSR, and 1 admin/service person.

Before automation:

- CSRs quote 3 to 4 commercial accounts daily each

- Agency writes roughly 130 to 160 new commercial policies per month (at ~25% close rate on ~600 monthly quotes)

- Renewals mostly auto-renew unmarketed

- Growth limited by CSR capacity; considering hiring #3

After automation:

- CSRs quote 12 to 15 commercial accounts daily each

- Agency writes roughly 300 to 375 new commercial policies per month

- Top 30% of renewals are systematically remarketed

- CSR hire delayed or repurposed to producer role

The agency's revenue capacity roughly doubles. The cost of achieving that? A few hundred dollars per month in software, not $55,000+ per year in salary and benefits.

Frequently Asked Questions

How much does quoting automation cost?

Commercial comparative raters range from free (Semsee's Essential tier, or through agency network partnerships) to $99–$499/month platform fees plus per-submission charges (QuoteSweep). Tarmika is approximately $225 per month flat for up to five users through association partnerships. Even at the highest price point, the cost is a fraction of a single employee's salary.

How long until I see ROI?

Most agencies see measurable time savings in the first week. The first month typically generates enough additional quoting capacity to justify the cost several times over. Full revenue impact compounds over 3 to 6 months as new policies bind and renew.

Will my team resist the change?

Some will, at first. The key is starting with willing adopters, showing real time-savings numbers from the first week, and not forcing the change on everyone simultaneously. See our automation guide for detailed adoption strategies.

Does this work for small agencies?

Small agencies often see the biggest proportional impact. A 2-person agency where one person does all the commercial quoting can effectively double their production capacity with a single tool. The growth potential relative to agency size is higher, not lower, for small shops.

What if I'm already using a comparative rater?

Evaluate whether your current tool covers your full carrier panel. If you're appointed with regional or specialty carriers that your rater can't reach, supplementing with an AI web agent-based tool (like QuoteSweep) can close the gap and further expand your quoting capacity.